![]()

If you work for yourself, the Solo 401k provides more investment options, the highest contribution limits, and the lowest fees of any fully self directed retirement plan.

Setting up a Solo 401k retirement plan is easy and allows for tax-deductible contributions much larger than an IRA or standard 401k. Plus it puts you in control with access to a world of alternative investment options.

Your Solo 401k makes you the CEO of your money with access to a full range of investment options so you can grow your money faster.

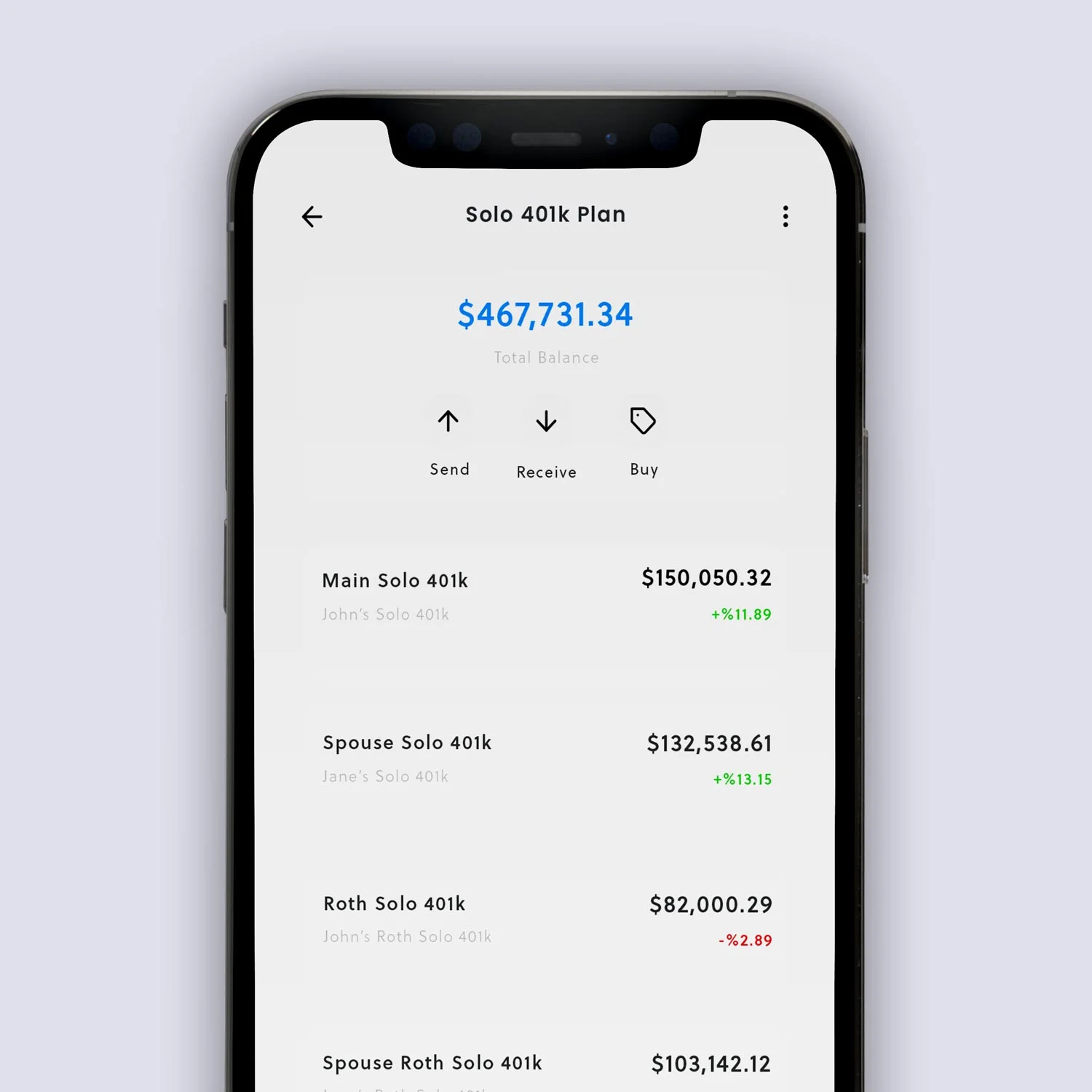

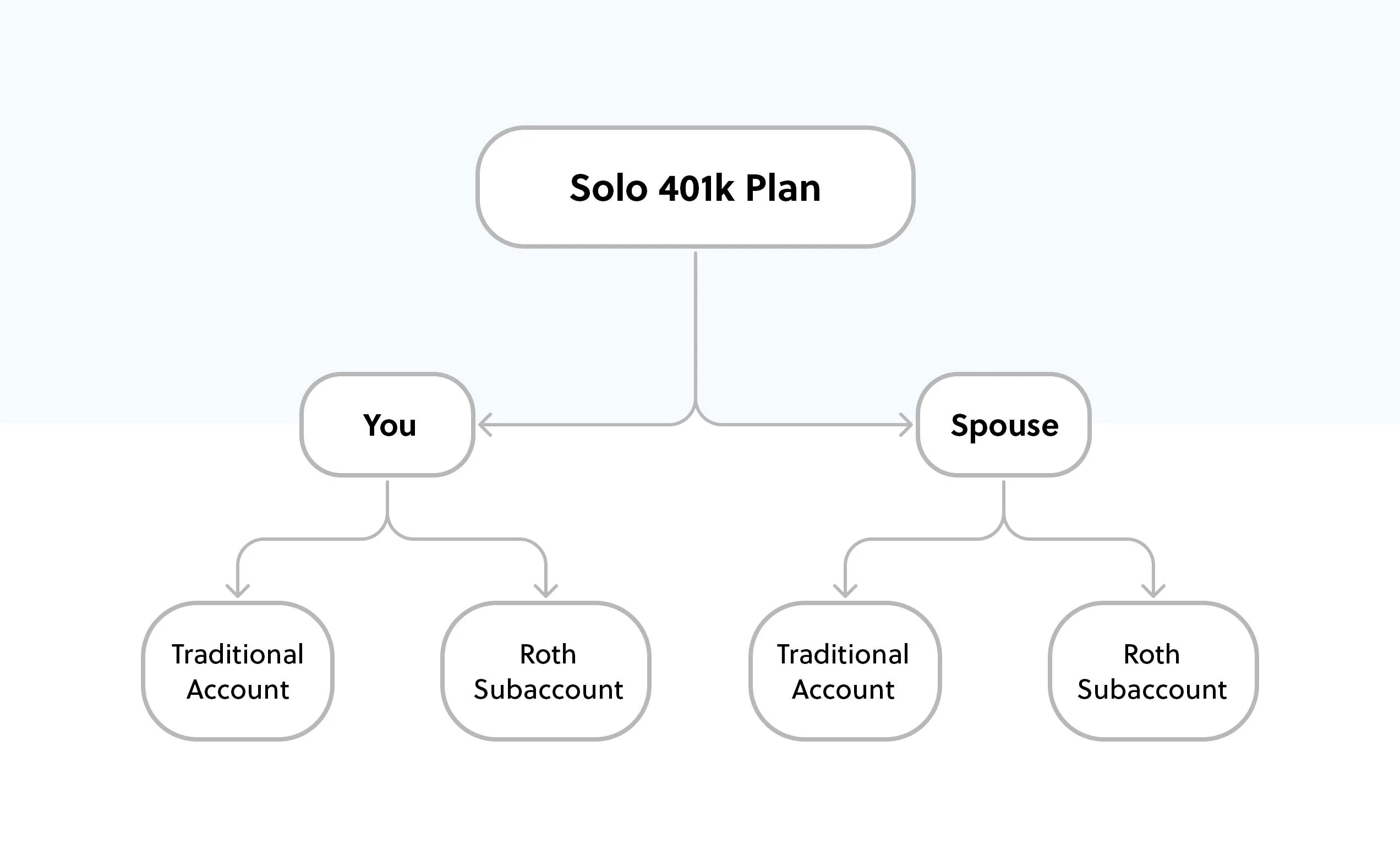

Your Solo 401k is four accounts in one, and there are no transaction fees or rollover fees.

Contribution limits are based on net earnings from self employment. The more you earn from self employment, the bigger the tax deduction you get for saving and investing for your future.

💸 Select Income Range $19,000 - $40,000 $40,000 - $80,000 $80,000 - $120,000 $120,000 - $150,000+ See If You Qualify Select Your Income Range

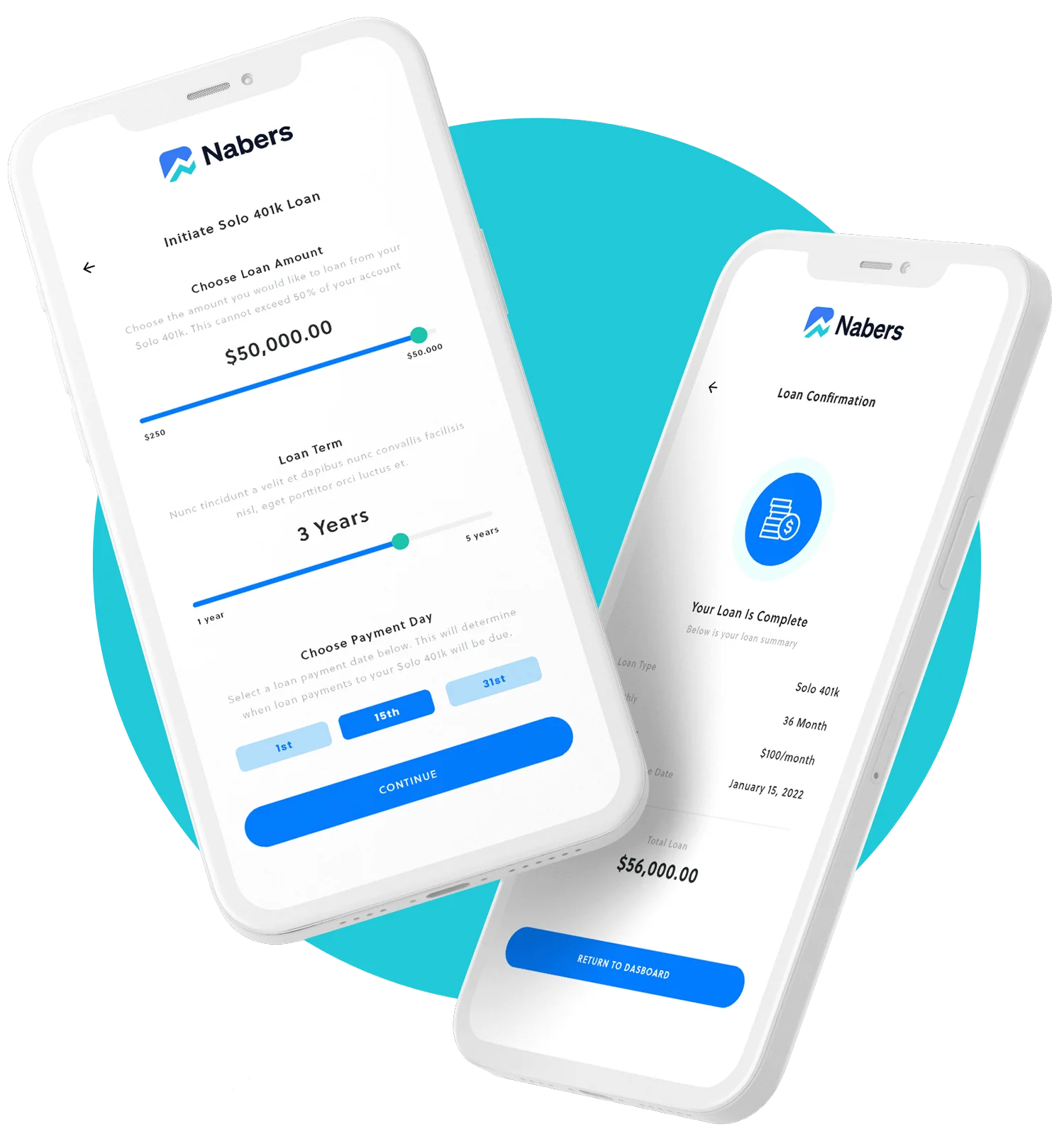

No credit check, no bank—instant approval—all from within your Solo 401k online dashboard.

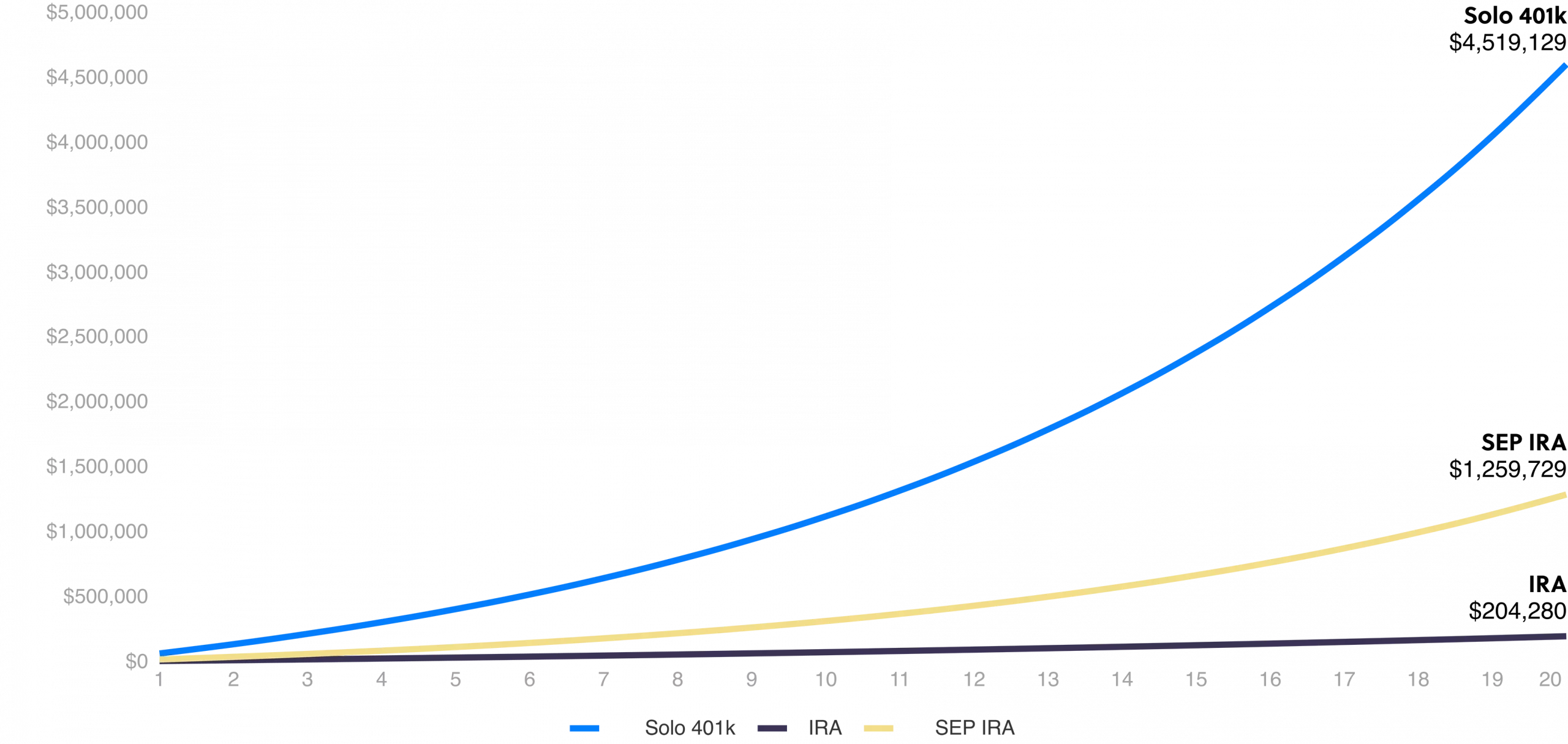

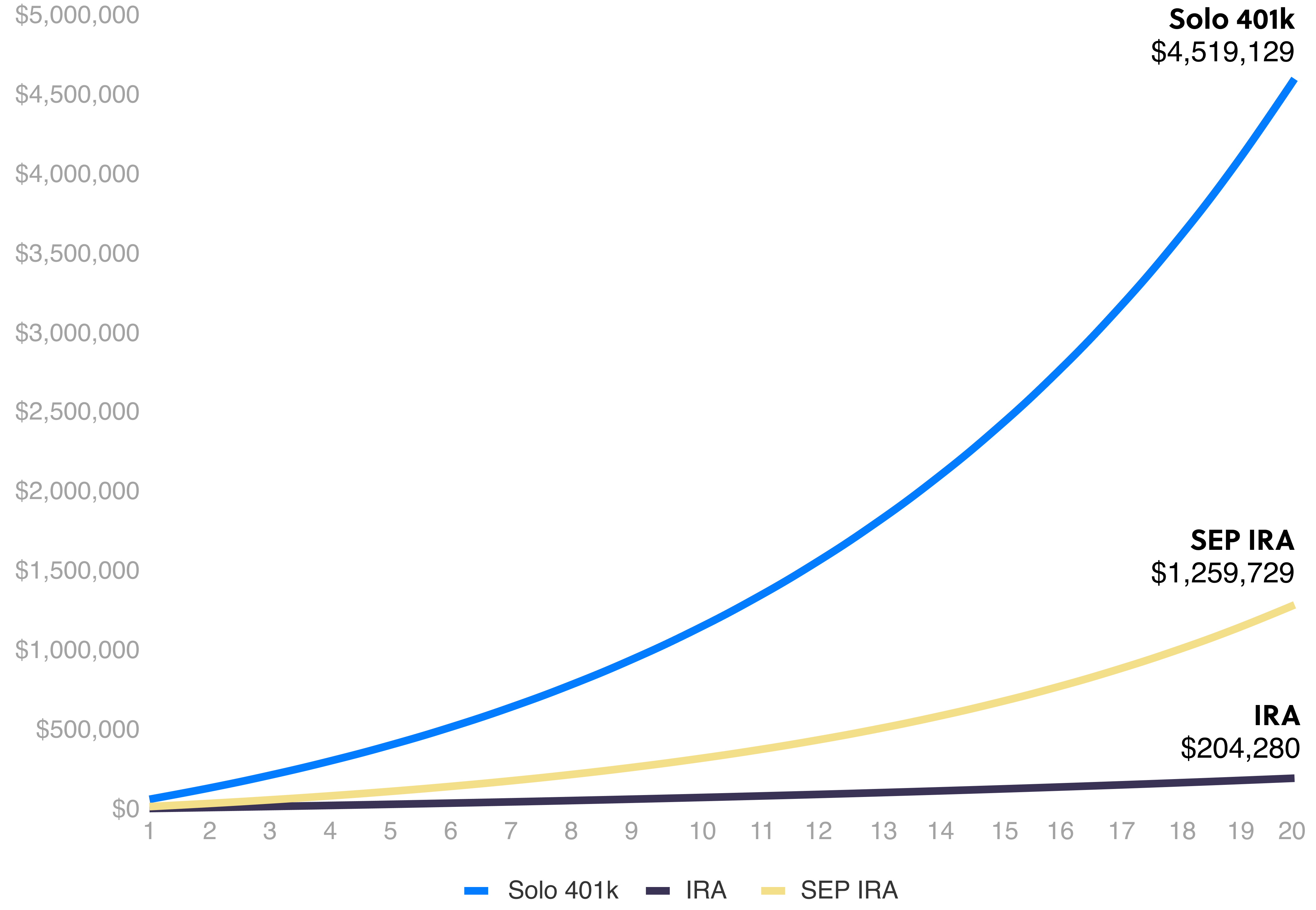

The difference this can make in your finances is significant due to the effects of larger contributions and a higher growth rate.

* Illustration assumes net earnings from self employment of $148,000/yr, maximum Solo 401k contributions of $56,000/yr and investment growth of 12%/yr with alternative investments; compared to maximum contributions into IRA of $6,000 and SEP IRA of $37,000 with compound annual growth rate equal to that of S&P 500 in 2000-2018, including dividends, which is 4.83%.

The Solo 401k is a special type of retirement plan for business owners (and their spouses). In many ways, the Solo 401k functions like a corporate 401k plan but allows you greater freedom to invest in what you want, and contribute on your own schedule because you are your own 401k plan administrator and trustee.

What do I need to qualify for a Solo 401k?There are two elements needed to qualify for a Solo 401k:

1) The presence of self-employment business activity and

2) the absence of full-time employees. Please see our page on Solo 401k

How long does it take Nabers Group to set up the Solo 401k?The application will only take you a few minutes. After you submit your application to us, we’ll have your documents prepared and delivered to your private encrypted 401k document dashboard in just a couple hours! You have access to your private 401k dashboard 24/7 so you can begin a rollover at 2 am without waiting for someone to have to send you any paperwork. However, the Nabers Group team is always a phone call, email or online chat away to answer any of your questions and make sure you’re well supported.

What can I rollover into the Solo 401k?You can rollover almost any type of retirement plan into the Solo 401k, including a traditional IRA, another 401k plan, 403b, pension plan, TSP, etc. The only retirement plan that cannot roll into a Solo 401k is a Roth IRA as per IRS rules.

Who helps me do the rollover?The Nabers Group team is here to help every step of the way. Our revolutionary proprietary software will help you complete and generate a rollover packet to send to your current custodian in 2 minutes or less. Your rollover packet includes all the relevant compliance paperwork proving your Solo 401k is an IRS-approved plan, including a copy of our IRS Opinion Letter, and even sample 1099-R so your custodian can document the rollover as a direct rollover.

Where do the rollover funds go? Does Nabers Group manage the 401k?You’ll receive a check in the mail for your rollover funds with the check made payable to your new Solo 410k trust. Nabers Group never touches your money so it’s safe in your hands as your own 401k trustee. Nabers Group is not a custodian so we don’t manage your investments. You are your own custodian, giving you full freedom and flexibility to invest your funds any way you choose.

Do I have to rollover everything?You can rollover a portion or all of your funds into the Solo 401k plan. It’s your choice.

Can I rollover assets or only cash?You can rollover cash and/or in-kind assets. Our rollover paperwork will give you a section to note if and how you’d like to rollover in-kind assets such as stocks, bonds, or even real estate.

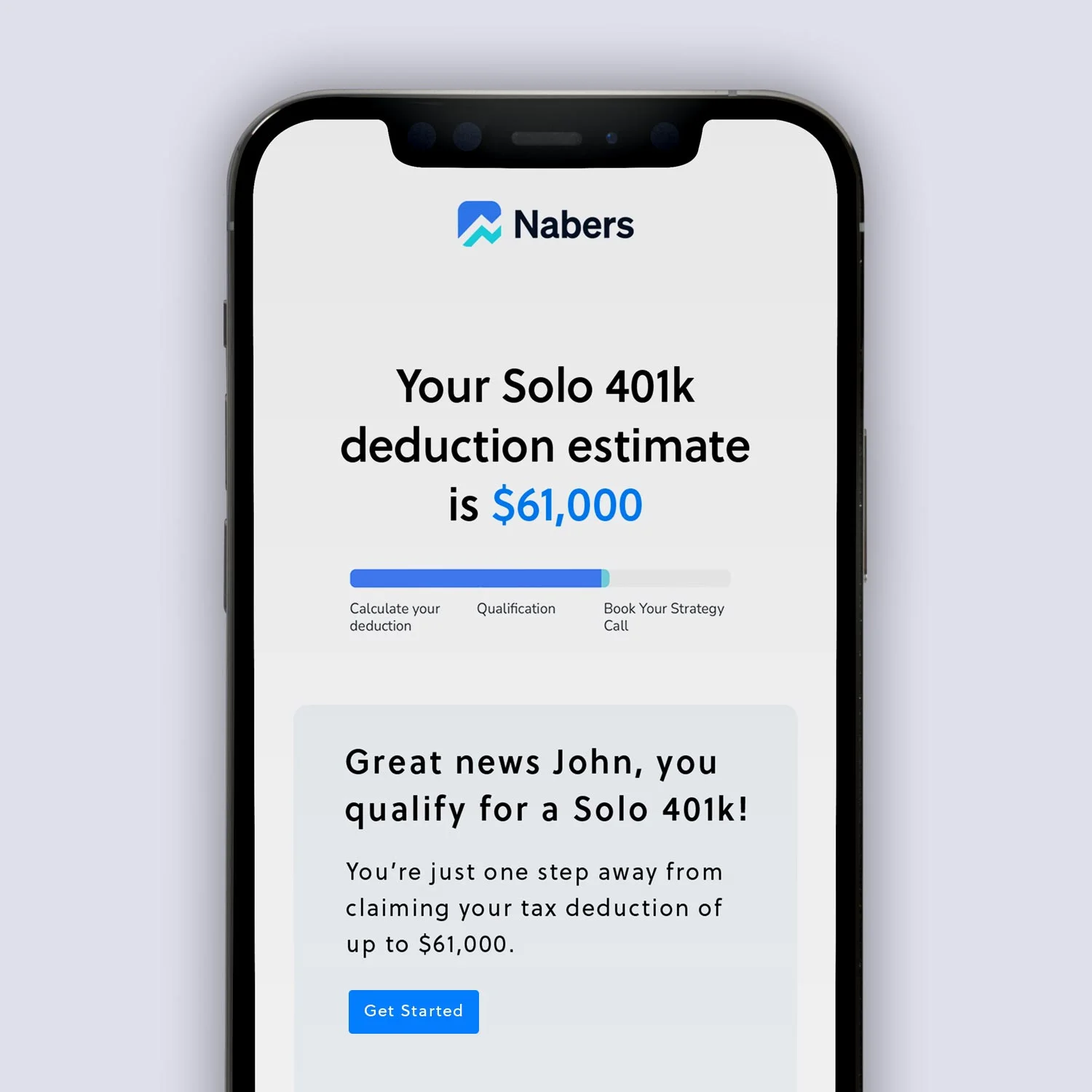

How much can I contribute to the Solo 401k?As of 2022, you can contribute up to $61,000 (or $69,500 if you are age 50 or older). If your spouse participates in the Solo 401k plan with you, double that contribution amount!

Can I have a Solo 401k and my corporate (regular) job at the same time? Can I contribute to both the Solo 401k and regular 401k plan at the same time?Yes! The Solo 401k has two types of contributions: employee (salary deferral) contributions and employer (profit-sharing) contributions. Your employee contributions are limited to $19,500 across all 401k plans (or $26,000 if you are age 50 or older). That means if you are contributing $10,000 to your regular 401k at work, you would be able to contribute the remaining $9,500 to your Solo 401k plan. Employer (profit-sharing) contributions stand alone so the amount you contribute to the employer portion of your Solo 401k plan does not affect your regular job 401k because they are two distinct employers/businesses.

Can I move funds into a new Solo 401k from an IRA or other 401(k)/457/403(b) retirement account?Yes! Ever since the Pension Protection Act was passed in 2006, you have the ability to do a tax free transfer, or “rollover,” of retirement funds from one retirement account to another.

Do I have to own a business to open a Solo 401k?You must meet 2 requirements to open a Solo 401k:

1) Entrepreneurship – This can be working as a freelancer, independent contractor, or business owner. This can be in the form of a sole proprietor or a formal corporation or LLC. Your entrepreneurship can be brand new, part time, or full time.

2) No full time employees – If you pay yourself a W2 paycheck that’s fine, but no outside W2 employees who work 1000+ hours a year.

What if my business has partners but no employees?No problem! We’ll write a special type of Solo 401k plan for you (for a small additional fee) where your business partner is excluded from participating in your plan. This allows the plan to remain truly “Solo”.

Can my spouse or I own a business that has full time W2 employees?No. If you or your spouse own a business that has W2 employees who work more than 1000 hours per year, you do not qualify for a Solo 401k account and the Checkbook IRA is the best type of Self-Directed retirement account for you.

Can my spouse participate in my Solo 401k too?Yes, it is possible for your spouse to participate in your Solo 401k, without having to create another Solo 401k plan. He/she will be able to rollover and contribute funds alongside you. This also means you and your spouse can combine your retirement funds for investments, which is illegal in IRAs.

What kind of paperwork does the IRS expect me to file?The Solo 401k is a retirement account and is tax-deferred, therefore there is no tax return due for a Solo 401k plan. Once you have $250,000 or more in total plan value (add up all your assets and cash in the plan), you will file form 5500-EZ. If you have less than $250,000 in your 401k plan, nothing needs to be filed. The Nabers Group team has guides and articles to guide you and your CPA through successfully completing this form. Our clients have told us that with the help of our trainings and guides, the 5500-EZ took them less than 10 minutes to complete!

What paperwork will Nabers Group provide me for setting up the Solo 401k?Yes, we were the very first non-custodial document provider in the industry and have been setting up Solo 401k plans since 2006 when the Solo 401k first came into existence. Your Solo 401k plan includes a copy of our IRS Opinion Letter proving our 401k plan and trust have been approved by the IRS. We work with the IRS and DOL on a consistent basis to ensure our documents are up to date and afford the greatest freedoms to Solo 401k accountholders while maintaining the strictest compliance standards.